Finally, the home stretch of the buying process: Closing! All inspections have been completed and the appraisal has been processed. This means the next steps for the buyers, sellers, agents and lenders is to work with the title company to become clear to close on the property. Closing is the formal process where a seller transfers ownership of the property to the buyers. After this final process, the buyer owns the home outright.

Finally, the home stretch of the buying process: Closing! All inspections have been completed and the appraisal has been processed. This means the next steps for the buyers, sellers, agents and lenders is to work with the title company to become clear to close on the property. Closing is the formal process where a seller transfers ownership of the property to the buyers. After this final process, the buyer owns the home outright.

On average, this process takes 30-45 days, but 60 day closings are not uncommon. The timeframe of this process is dependent on when the buyer wishes to gain possession, when the seller is willing to vacate and if there were any issues during the inspection period.

Get an Updated Loan Estimate

During the initial loan attainment, the lender likely provided a loan estimate (LE), which included the mortgage amount, monthly payments, insurance fees, and any additional fees associated with the closing including title insurance and closing fees. Be sure to attain an updated LE halfway through the buying process and compare numbers. Usually, about a week before the closing, the title company will provide a Closing Disclosure (CD) that breaks down the updated fees for the buyer and seller. If there are any questions or discrepancies, now is the time to ask/amend. Remember that a CD:

- Is Required to be Provided to the Buyer & Seller at Least 3 Days Prior to Closing

- Includes All Loan Terms, Projected Monthly Payments, Closing Costs & Fees

Not sure what all the details are on the CD? Use this interactive closing disclosure explainer.

What Is Title Insurance?

The term “title” refers to the collected ownership records of a piece of real estate, including the transfer of any property rights, and any loans using the property as collateral. A clear line of title makes you much less vulnerable to ownership claims from other parties and to outstanding debts of previous property owners. This is part of the closing fees and essential to ensure no other person has claim to the property.

*Note: The title company can be a separate entity from the settlement company, but is often the same organization.

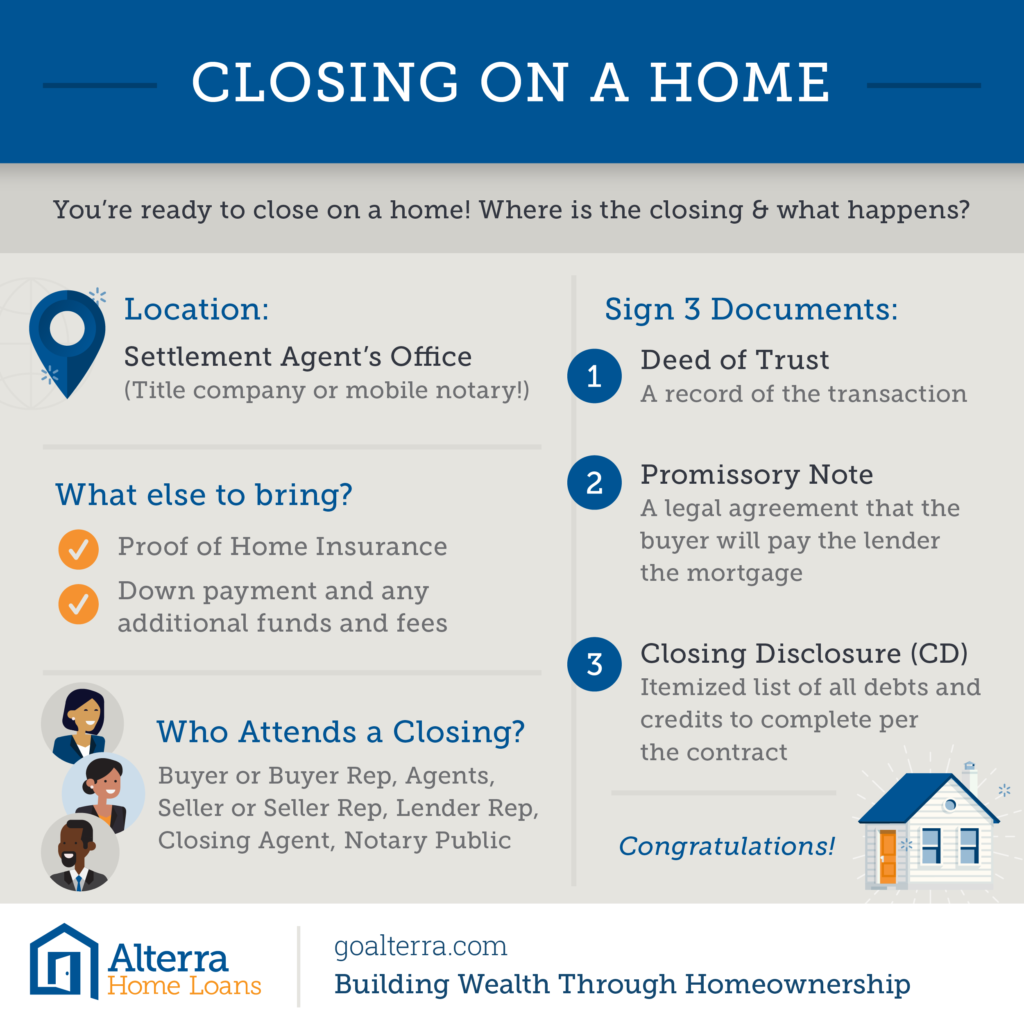

Where Is the Closing & What Happens?

A closing typically occurs at a settlement agent’s office, which can be at the title company’s office or executed by a mobile notary as well. Typically, three documents are signed:

- Deed of Trust: A deed is the records with the local Clerk of Courts of the transaction and the mortgage lien on the property now owned by the buyer.

- Promissory Note: A legal agreement that the buyer will pay the lender for the mortgage principal, plus the agreed upon interest, as well as where fund are to be sent.

- Closing Disclosure (CD): The itemized list of all debts and credits to complete the closing that are associated with the contract.

If documentation of homeowners insurance has not already been provided, it must be provided at closing. If the down payment and funds for closing have yet to be received, this must be provided at closing as well. This is typically 2-5% of the home’s value and can include recording fees, loan origination fees, notary fees title insurance and homeowners insurance.

Who Attends a Closing?

- Buyer or Buyer Rep

- Agents

- Seller or Seller Rep

- Lender Rep

- Closing Agent

- Notary Public

Not all are required to attend and the selling party can sign in a different location than the buying party. This is very typical when one of the parties lives in a different state or during a VA loan closing.