Buying a home is viewed as a symbol of the “American Dream” for many and provides a sense of security in an often-unstable economy. Many desire this, but are not sure if it is a tangible financial investment that can turn into a profitable venture long-term. Understanding the meaning of wealth can help you make the entire process more reassuring in the long run.

Buying a home is viewed as a symbol of the “American Dream” for many and provides a sense of security in an often-unstable economy. Many desire this, but are not sure if it is a tangible financial investment that can turn into a profitable venture long-term. Understanding the meaning of wealth can help you make the entire process more reassuring in the long run.

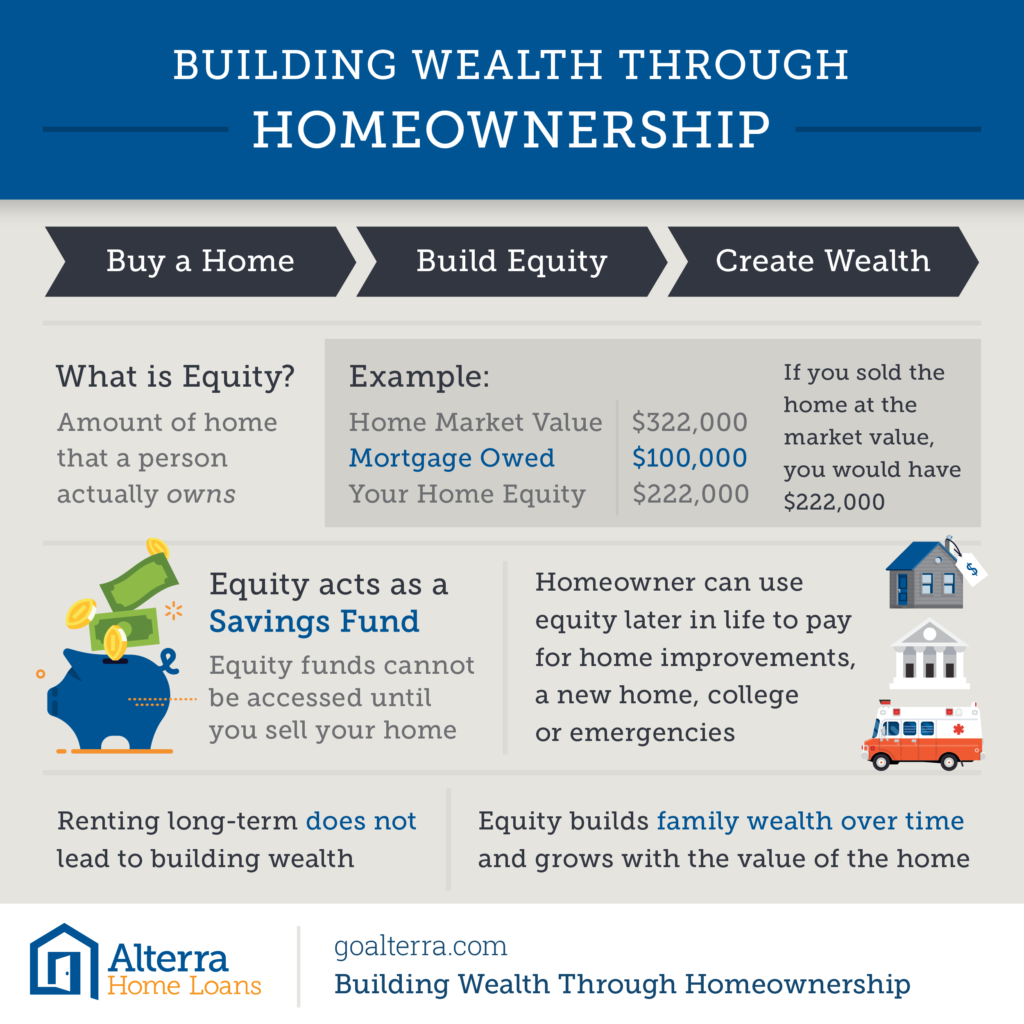

What is Equity?

Equity is the amount of home that a person actually owns. This total is not the mortgage amount, but loan balance subtracted from the value of the home. If this number is positive number, congratulations, there is equity in the home and therefore wealth. If the number is a negative number, then the buyer will likely owe if the home is sold and be indebted at the sale.

Example:

Home market value $322,000

Mortgage Owed $100,000

Your Home Equity $222,000

If you sold the home at the market value, you would have $222,000.

This value can fluctuate dependent on the market, but statistically stays within a 10% average, making homeownership a smart choice. Equity is valuable to the consumer because a homeowner can use these untouchable funds later in life to pay for burdens or unforeseen costs such as home improvements, a new home, college or emergencies. This of the home as a savings fund that will not be touched until the transfer of ownership.

Overall, this is a popular way to increase wealth because the net worth of the family increases over the years. According to the Federal Reserve, the median net worth of a homeowners in 2016 was between $225,000-$230,000. For families that rent, the average net worth was $5,000.

How Does Equity Grow

Equity grows with the value of the home, not just the amount paid down by the homeowner. If a home is in the right market, values can increase as the area becomes more desirable, increasing the property value and the equity margin. For example, if a home is appreciating at a rate of 4% per $10,000, this can be leveraged from a $10,000 investment to a $100,000 investment.

Benefits to Homeowners

- Forced savings: This is a way to create a steady savings without having the cash in hand to put into a savings account. For buyers who may have a hard time putting money aside for the future, this is a great way to save funds without manually putting the money aside.

- Value Versus Renting: People who rent have nothing to show for their payments towards a property when they depart a home. This is the downside to renting. Renting is great in the short-term, but provides zero benefits to most Americans when trying to save for wealth.

When weighing the pros and cons to a home purchase, consider long-term goals. If a goal for the family is to save for future needs, purchasing a home in the right market can make profits that outpace even the stock market. Weigh the options and choose what is best for the family by discussing the decision with lenders, agents and family.